While cities around the world are debating (or arguing) about global climate change, one of the most significant barriers to lowering carbon emissions is in the construction industry. While transportation and electricity are the primary drivers of carbon emissions, construction is also a significant contributor to greenhouse gas emissions. That doesn’t only refer to carbon emissions from generators and gear. The embedded carbon in materials is also a significant carbon producer; cement alone could account for 8% of global carbon emissions.

Limiting construction operations could be the simplest answer. But, like driving and producing power, it’s unlikely to happen, especially given the tremendous demand for space throughout the world today. A different strategy is to utilize materials with lower embodied carbon. However, when construction materials contain embodied carbon due to their physical constituents as well as the effort required to assemble them into usable shape, this can be a tough proposition. Carbon monitoring often receives the short end of the stick for contractors and project managers who are already preoccupied with avoiding delays or cost overruns.

Understanding embedded carbon is critical for reducing carbon emissions, especially for firms that have signed climate change treaties. These tools have a real chance to help visualize and, as a result, reduce carbon emissions, even when they are difficult to detect. However, for corporations that haven’t committed to combating climate change, simply recognizing the carbon content of certain construction materials is unlikely to have a significant effect.

As a result, governments should consider providing financial incentives for low-carbon construction. According to several studies, industry programs such as LEED certification may do little to help accomplish energy reduction goals; it’s not unreasonable to believe that the same is true for embodied carbon. Cities may enjoy net profits from carbon reduction programs if governments provide incentives such as a tax credit for the use of low-carbon materials.

A Call for Action

As one of the world’s leading economic sectors, the construction industry has a significant role to play in reaching global sustainability goals. While the industry isn’t known for being a leader in terms of sustainability, the entire ecosystem appears to be evolving. The COVID-19 pandemic will almost certainly play a role in this, not least because it will hasten reform. In this context, we must begin to combine the necessary thinking and planning to develop far stronger economic and environmental resiliency in order to battle environmental dangers.

Environmental, social, and governance (ESG) factors are critical indicators of a company’s long-term viability and social implications in the construction industry. Metrics can be evaluated across the entire ecosystem as well as the life cycle of buildings and infrastructure. The environmental component addresses issues such as air quality and energy management and the impact of a project on biodiversity, waste, and water management. Though it’s difficult to assign Greenhouse gases across the construction ecosystem, certainly, construction is directly or indirectly responsible for about 40% of world CO2 emissions from fuel burning and 25% of total Greenhouse gas emissions.

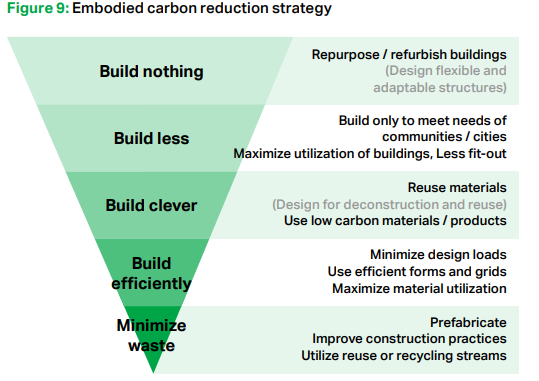

Two constituents primarily drive the construction ecosystem’s Greenhouse gas emissions: raw-material processing for buildings and infrastructure (about 30precent of overall construction emissions annually, mainly cement and steel) and building operations (around 70%). We cannot wait to replace products at the end of their life cycle if we are to achieve decarbonization thresholds by 2050, considering the standard asset lifespans of 30 to 130 years. With approximately 80percent of the projected building stock for 2050 already in place, there is a significant need — and opportunity — to reconfigure current assets.

The raw material contribution is largely from energy-intensive cement production and metals (approximately half of world steel production is used for construction), which account for nearly 7% of total Greenhouse gas emissions. Commercial and residential building operations contribute primarily through space and water heating within buildings, heat leakage due to poor insulation, and other energy consumption such as lighting, air conditioning, and appliances.

The most important aspect in defining Greenhouse gas emissions over the life of a structure is its design. The majority of decisions concerning the project’s Greenhouse gas emissions have already been made by the time construction begins. Early in a project, before construction begins, the capacity to impact a building’s lifetime emissions is greatest. Key design choices, such as new construction versus renovation, building size and shape, insulation level, and floor-space flexibility, can have a long-term impact on emissions.

If unmanaged, the construction ecosystem’s carbon footprint would rise over the next 30 years as we try to fulfill the demands of a growing population and urbanization. On the plus side, this creates chances to optimize new construction, while a concurrent transition toward renewable energy will assist in reducing emissions. With power-system decarbonization expected to reduce emissions by 2050, the requirement to remove yearly emissions for the construction and real estate ecosystem to meet the 1.5-degree warming target set by the Paris Agreement in 2016 remains critical.

Nonetheless, decarbonization will be tough. It is a fundamental aspect of this process to incentivize stakeholders across the value chain to work together. The construction industry is undergoing a transformation that is altering the entire sector. Another problem is deploying smart technology across millions of locations in an industry with the second-lowest level of digitalization and sluggish productivity growth.

The scope of the problem and the obstacles that each stakeholder in the ecosystem faces are enormous. But the good thing is that each player may take specific steps to significantly reduce its carbon footprint—and many of these steps will also save money. But, if the sector aims to attain its ultimate aim of net-zero emissions at an ecosystem level, a concerted effort across existing and new building stock will be required.

No single stakeholder can fix the emissions challenge on their own. With several steps in the product life cycle, the construction industry is highly fragmented. Though every stakeholder in this complex ecosystem has the potential to make a difference and seize opportunities, joint efforts among multiple stakeholders are more likely to produce the best outcomes.